Two Companies I Think The Market Is Mispricing (AT.L, PPIH)

Ashtead Technology delivers FY25 results ahead of expectations at 8x earnings. Perma-Pipe quietly pivots into AI data center infrastructure while growing revenue 37%. Both benefit from the same struct

To read our full disclaimer, click here.

On the surface, Ashtead Technology (AT.L) and Perma-Pipe International (PPIH) look like very different businesses.

One rents subsea equipment to offshore energy contractors. The other manufactures pre-insulated piping systems for oil & gas, district energy, and increasingly, data center cooling.

But they share a common thread: both are infrastructure picks-and-shovels plays sitting at the intersection of energy security and industrial buildout, and both are being undervalued by a market that’s fixated on the wrong risks.

Ashtead just delivered full-year results that beat expectations. Perma-Pipe announced a strategic expansion into AI data center infrastructure while growing revenue 37% year-to-date.

Let’s start with the numbers.

Part 1: Ashtead Technology - FY25 Full-Year Results (AT.L)

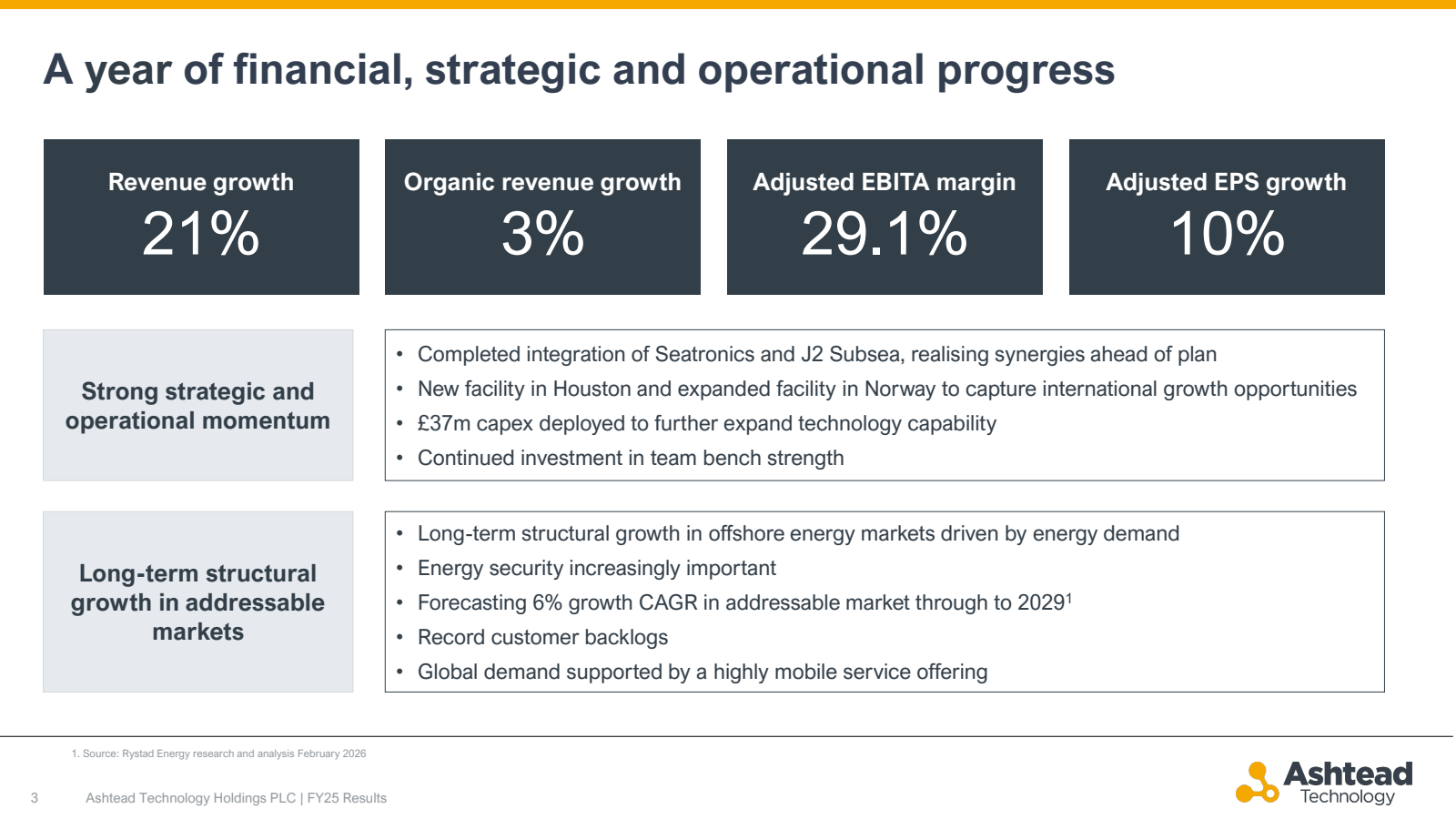

Ashtead Technology released its full-year results on 17 March.

The headline: adjusted EPS came in at 49.4p - 10% ahead of the 44.7p consensus I referenced in our January update. Margins hit the top end of management’s target range. The balance sheet strengthened materially. And the backlog picture is the strongest it’s ever been.

At 403p, the stock trades at roughly 8x trailing earnings.

For a business that has compounded adjusted EPS at a 37% CAGR since 2022, that multiple feels mispriced to me.

The Numbers

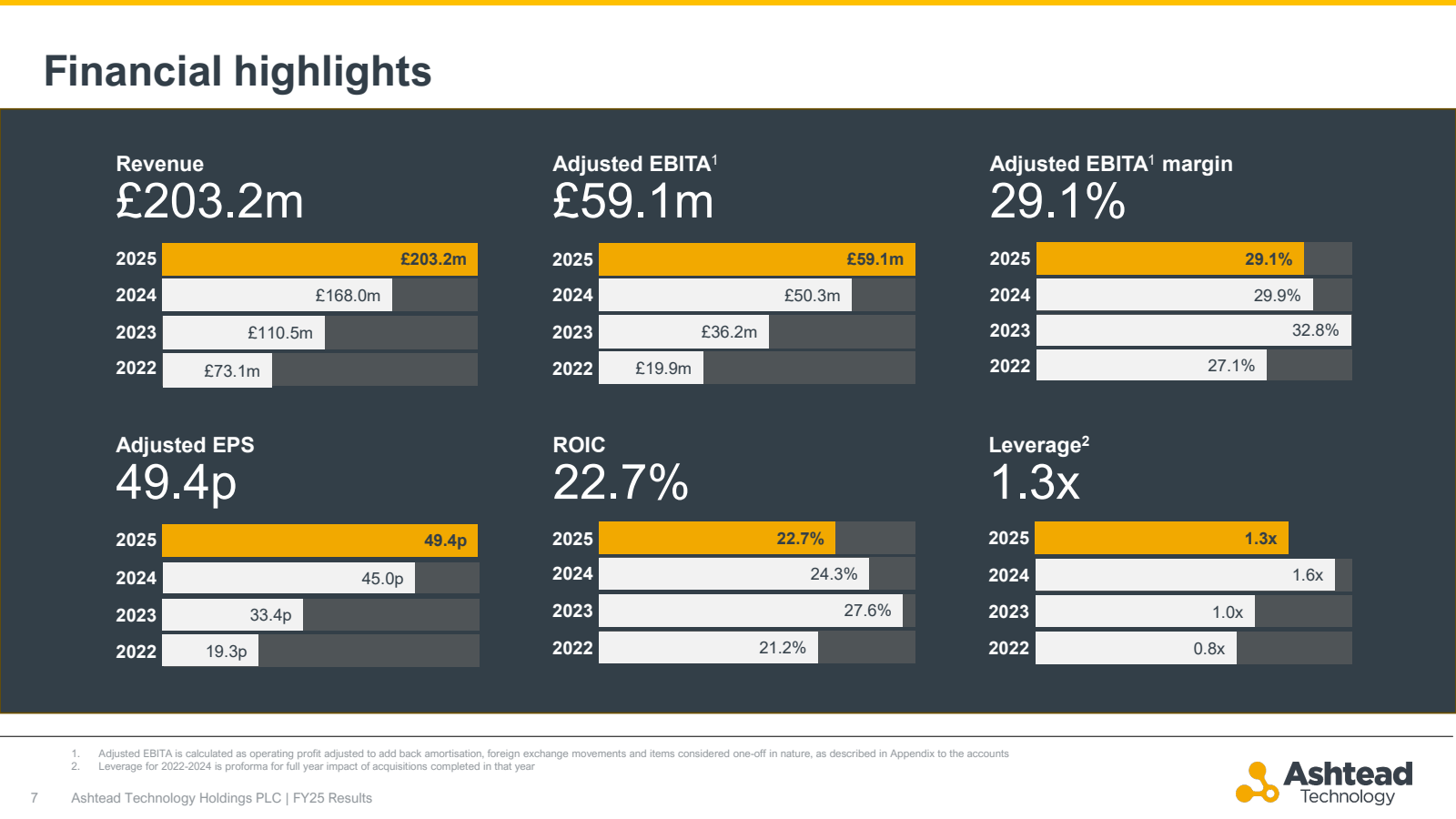

Full-year revenue came in at £203.2 million, up 21% year-on-year. The breakdown: 19% from the Seatronics and J2 Subsea acquisitions completed in late 2024, 3% organic, and a 1% FX headwind.

Management deliberately trimmed lower-margin activities inherited from the acquisitions, prioritising earnings quality over top-line vanity.

The result: Adjusted EBITA of £59.1 million, up 17.5% year-on-year, with a 29.1% margin - towards the top end of management’s medium-term target range. That beat the £57.7m consensus expectation.

Adjusted EPS of 49.4p was up 10% on the prior year. Statutory diluted EPS hit 39.6p, up 12%.

ROIC came in at 22.7% - down from 24.3% last year due to the acquisition mix, but still well above cost of capital.

Cash generation was strong. Cash inflow from operations was £73.2 million (2024: £46.5m). After capex of £37.2m, free cash flow was £40.4m, representing an EBITDA-to-free-cash-flow conversion ratio of roughly 49%.

Leverage dropped to 1.3x net debt to EBITDA at year-end, down from 1.6x proforma at the start of the year. Net debt fell to £108.9m from £128.4m.

The dividend increased 8% to 1.3p per share. The Board acknowledged potential for share buybacks alongside continued M&A, noting buybacks are a lower priority given the growth opportunities ahead.

In the rest of this post, I discuss:

What the Ashtead earnings call revealed about backlog visibility and the M&A flywheel

Why the Middle East situation is actually a tailwind for Ashtead, not a headwind

Perma-Pipe’s strategic pivot into AI data center infrastructure

Why both companies sit on the right side of the same structural trends

Updated valuation and positioning