The Pyramid: How I Actually Build a Portfolio

A companion piece to this month's portfolio update. The trades only make sense if you understand the structure they serve - so here's my structure, written down properly.

To read our full disclaimer, click here.

There’s a question every concentrated investor eventually gets asked: if you believe in concentration, why do your new positions start so small?

It looks like a contradiction. It isn’t. And resolving it is the single most important idea in how I now build a portfolio:

Concentration is the end state, not the starting position. Size is earned, not assigned.

This post walks through the whole framework - the tiers, how positions move between them, and why that movement is really just “cut your losses, let your winners run” built into the structure instead of left to willpower. Then, for paid subscribers, I’ll show you exactly what my own pyramid looks like right now, name by name, and why I’m running a more concentrated version than the textbook.

Why structure matters more than stock-picking

Microcap returns don’t arrive evenly.

They follow power laws: over any meaningful period, a small handful of positions drives nearly all of the return, a larger group does roughly nothing, and a few lose money.

The uncomfortable truth is that you can’t reliably know in advance which position belongs to which group.

Research improves your odds - that’s the job - but certainty isn’t on offer at the moment you buy.

So the portfolio has to be built as a discovery machine rather than a set of finished convictions.

Many small bets at the bottom. Capital flowing toward whichever ones prove themselves. Mistakes dying cheaply before they can do real damage.

The structure does as much work as the stock selection.

Here’s the shape I’m aiming for:

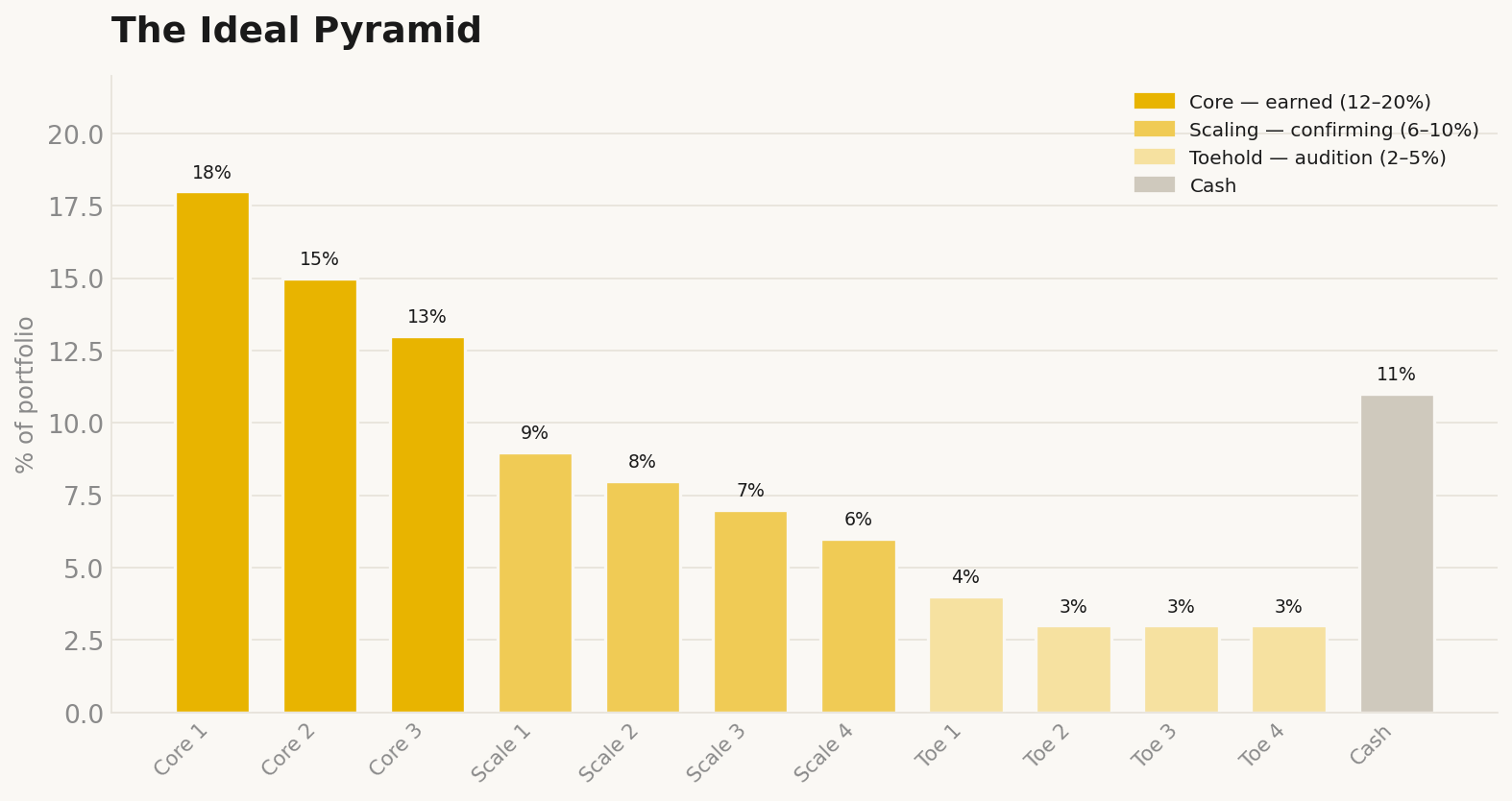

The three tiers

Toeholds (2–5% each): Auditions. A new idea enters here no matter how excited I am, because excitement at the point of purchase is the least reliable signal in investing. The position is small enough that a total thesis failure - down 40%, idea dead - costs the portfolio one or two percent. Every toehold gets written promotion criteria on day one: the specific, dated milestones that would justify buying more.

Scaling positions (6–10% each): A toehold gets promoted here when the business - not the share price - confirms the thesis. Contracts land, margins progress, management does what it said. This is where averaging up happens, often at prices above the original entry, which feels wrong and is right. Paying more for a company that has removed uncertainty is a better trade than paying less for one that hasn’t.

Core positions (12–20% each): The earned weights. Nothing arrives here by purchase alone - positions reach the core through years of execution compounded with appreciation. In a healthy book the top three to five names might be 60% of the portfolio, and the honest answer to “isn’t that risky?” is that the market built that concentration by rewarding the positions that deserved it.

Cash (5–10%): Dry powder. Its job is funding promotions and buying drawdowns - the moments when having capital available is worth far more than the drag of holding it.

How positions move - and why the movement is the philosophy

Everyone repeats the old line:

Cut your losses, let your winners run.

Almost nobody builds it into their portfolio’s actual mechanics. The pyramid does, in both directions.

Cutting losses happens at the bottom, where it’s cheap.

Lee Freeman-Shor’s research in The Art of Execution found that the investors who underperform aren’t the ones who pick bad stocks - they’re the ones who freeze when a position drops.

His rule: when you’re down, you either buy more with conviction or you sell. Holding and hoping is the one forbidden move.

The pyramid enforces this, because every position below the core is permanently on trial. At each review, everything gets classified as promote, hold, or prune - and “hold” has to be an active choice with a reason, not a default.

When a toehold fails its audition, the loss is capped at audition size. You take many small risks to discover the few worth taking a big one on.

Letting winners run happens at the top, automatically.

When a scaling position doubles, it promotes itself - no buying required.

And here’s the discipline that matters most: I don’t rebalance it away.

To hold a multibagger you have to actually hold it - through the 50% pullbacks, through the quarters where the price goes nowhere while fundamentals backfill, through every urge to bank the gain.

A core position only gets trimmed for two reasons: the valuation has pulled three or four years of future returns into the present, or it fails the pain test - could I hold through a 40% drawdown in this name without it breaking me or the portfolio? “The percentage looks big” is not on the list.

A large winner is the reward for being right, not a problem to tidy away.

Put the two halves together and you get the deepest property of the structure:

The asymmetry of the portfolio mirrors the asymmetry of the individual bets.

Downside capped small at the bottom; upside uncapped at the top. Each position is chosen for limited downside and uncapped upside - and the pyramid applies that same payoff shape to the whole book.

One more rule that follows from all of it: spend twice as much time on maintenance research - the companies you already own - as on hunting new ideas.

What you don’t own can’t hurt you. The promotion decisions are only as good as your ongoing knowledge of the businesses being judged.

In the Rest of This Post

Behind the paywall, for paid subscribers:

A chart of my actual portfolio mapped onto the pyramid - every position, every tier

Why I’m running a more concentrated version than the template, and how that happened

The one position carrying a core-sized weight it hasn’t fully earned yet

How a real prune this month proved the structure works as designed

A link through to where you can read about the companies themselves