The Most Asymmetric Bet We've Ever Made

20% of Our Portfolio, 2 Weeks to Resolution, and a Setup Where Heads We Win, tails We win More

To read our full disclaimer, click here.

Since our last thesis post, we've sized the following position to over 20% of our portfolio.

We said the catalyst day was July 7th - the deadline for a firm offer or walk-away decision.

Things have changed, and this is our update.

The deadline has been extended but here's what most investors are missing: this wasn't the acquirer stalling for time.

The target company's Board explicitly stated that "constructive discussions are advancing" and continuing engagement is "in the best interests of shareholders."

Our translation: The Board believes a deal is getting done.

This extension gives us more time to build our position if the stock drifts lower on the uncertainty.

With anticipated deal pricing between up to 20% above current levels, any weakness from impatient traders becomes our opportunity.

If the deal goes through, we're looking at a clean return in weeks.

If it doesn't, we're left holding one of the best-run companies in fintech.

A founder-led machine, trading at a cheap multiple, throwing off real cash, with plenty of reinvestment opportunities and buybacks underway.

That's not a loss.

That's a blessing.

📌 Heads we win. Tails we win more.

For full access to the deep dive, our fair value estimate, the acquisition mechanics, and why we think this business still doubles even without the deal, we’re offering a 25% weekend-only discount on our yearly plan.

You can get that here if you want:

What’s Changed

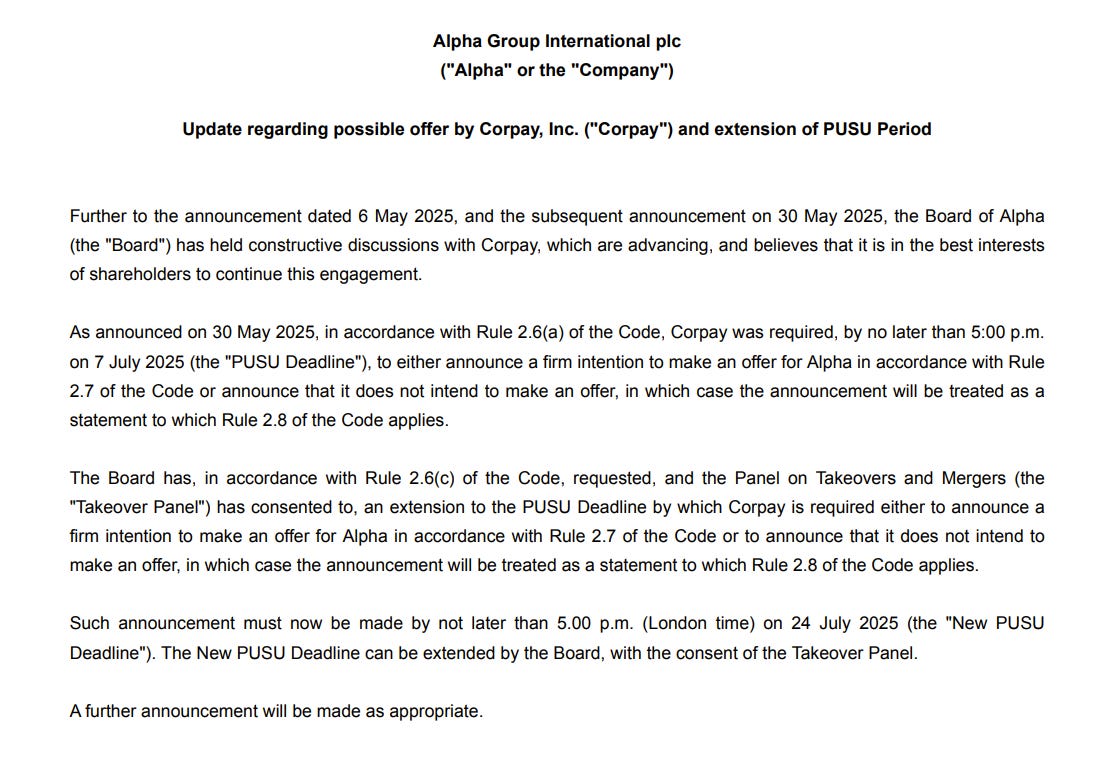

Corpay remains in active discussions to acquire Alpha, though the timeline has shifted beyond initial market expectations.

While many anticipated an announcement by July 7th, recent developments suggest something more significant is brewing.

The plot thickened when Alpha announced an extension of the PUSU deadline to July 24th.

But here's the crucial detail that many are missing: this wasn't Corpay buying time to decide if they want to proceed.

Alpha's Board explicitly stated that "constructive discussions with Corpay...are advancing" and that continuing engagement is "in the best interests of shareholders."

Here is the full press release:

Our translation: The Board believes a deal is getting done, and they're actively facilitating it.

We now anticipate deal pricing between 3,500 and 4,000 pence per share.

With Alpha currently trading around 3,360p (already up 5% from our entry) much of the takeover anticipated premium has been priced in, reflecting growing market confidence.

Our stance: We'll add to positions if the stock retreats closer to our original purchase price, but we're not chasing it higher.

We want our margin of safety to stay intact, especially knowing there's a chance of a meaningful pullback if negotiations collapse.

We're patient buyers here, willing to let the market come to us rather than paying up for what's already priced in.

For any new subscribers, here's our original analysis that explains the full details of this company.

What the Business Actually Does

Alpha Group International (LON: ALPH) is not your typical fintech.

They have built a modern financial platform designed to solve real-world complexity for institutional clients.

They are not chasing trading volume or transactional FX.

They are providing embedded infrastructure for companies and funds with cross-border financial needs.

The business operates across three core divisions.

1. Corporate Solutions (47 percent of revenue)

Alpha works directly with CFOs to manage currency risk. Clients include mid-sized manufacturers, tech firms, and service businesses with multi-currency exposure. These companies do not need low spreads. They need help managing uncertainty.

Alpha builds bespoke hedging strategies, models risk scenarios, and acts more like a financial partner than a broker. The average revenue per corporate client has grown to £71,000. Client count reached 974 in 2024. Both figures continue to rise steadily.

2. Alternative Funds and Private Markets (51 percent of revenue)

Alpha provides accounts, payments, and FX infrastructure for over 7,100 funds. These include private equity, real estate, and hedge funds operating across multiple jurisdictions.

These clients use Alpha to manage working capital, payroll, supplier payments, and investor distributions. Alpha earns both from service fees and the idle cash held in client accounts. These are not investment funds. They are operating balances.

This business generated £69 million in revenue last year, up 20 percent year over year. It continues to scale without material increases in cost.

3. Cobase (2 percent of revenue)

Cobase is a treasury management system that allows businesses to manage their accounts across different banks from a single interface. Alpha acquired it in 2023. Since then, revenue is up 70 percent. It adds both product depth and client stickiness.

Why the Business is Durable

Alpha does not compete on spread or price. They do not chase the largest trades or the easiest clients. Their model is high-trust, high-involvement, and built around long-term client retention.

Once Alpha is integrated into a client’s treasury function, the cost of switching is meaningful.

That creates durable relationships and pricing power.

It also means that new business comes from referrals, not advertising.

The Float Economics

Alpha now holds an average of £2.15 billion in client operating balances. This generates more than £80 million per year in interest income.

The cost to service these accounts is low.

There is no credit risk.

The income is recurring and scales with client growth.

This income does not show up clearly in adjusted EBITDA.

But it is cash.

And it makes up the largest single component of Alpha’s free cash flow.

This is the heart of the business.

As long as Alpha keeps adding new clients and new funds, this float will continue to grow.

Valuation

The company now trades at a market cap of ~£1.3 billion. Net cash on the balance sheet is approximately £250 million. That gives an enterprise value of £1.05 billion.

Free cash flow in 2024 was £90 million. T

his puts the business at 11.7 times EV to FCF.

That is low for a founder-led company with 80 percent gross margins, likely to grow revenues at 10-15 percent per year, and expanding globally with no debt.

Using a simple discounted cash flow:

Free cash flow: ~£90 million

Growth rate: 15% per year

Discount rate: 10%

Terminal multiple: 16x

This produces an intrinsic equity value of between £1.9 and £2.0 billion, or 4,500 to 4,600 pence per share. That implies 40 to 50 percent upside from today’s price of approximately 3,080 pence.

Now listed in the FTSE 250, Alpha is beginning to gain broader institutional attention.

However, we believe the full cash generation and long-term economics are still misunderstood by the wider market.

Capital Allocation

Alpha is internally funded.

There is no debt.

No dilution.

No dependence on capital markets.

In 2024, the company repurchased £30 million of its own stock. It pays a small dividend to satisfy institutional mandates. But most capital is reinvested into people, product, and technology.

The founder, Morgan Tillbrook, is now Chairman. He remains involved in strategy and culture. The new CEO was promoted internally. Insider ownership remains above 13 percent.

Incentives are aligned.

The culture is intact.

The Bottom Line

Alpha is one of the most attractive businesses in the UK public markets. It combines:

Consistent, recurring revenues

Low churn and high margins

Strong free cash flow and no debt

Clear reinvestment paths across Europe

Insider ownership and disciplined capital allocation

And a possible takeover catalyst in the near term

Fair value sits 40 to 50% above today’s share price.

That does not include the ongoing compounding of free cash flow per share.

We are long Alpha and continue to add.

We hope you found this valuable. Have a great rest of your weekend.

Dom

Schwar Capital

Disclaimer: The content provided in this newsletter is for informational purposes only and does not constitute financial, investment, or other professional advice. The opinions expressed here are those of the author and do not necessarily reflect the views of Schwar Capital. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. The author may or may not hold positions in the stocks or other financial instruments mentioned. Always do your own research or consult with a qualified financial advisor before making any investment decisions. You can see our full disclaimer here.