March Portfolio Update

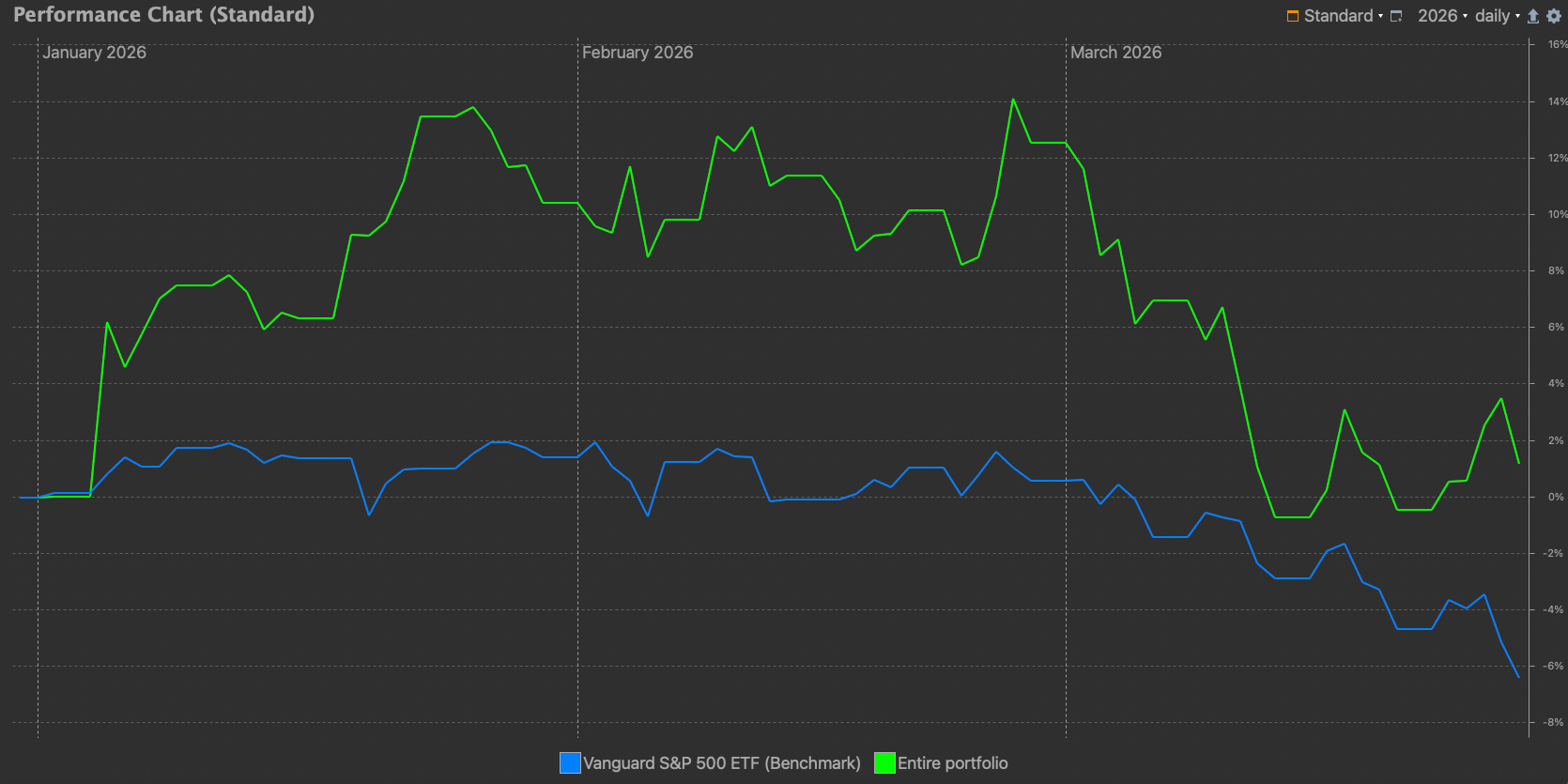

Up 1.2% year-to-date versus -6.4% for the S&P 500. Here's what I'm doing...

To read our full disclaimer, click here.

The SCR portfolio is up 1.2% year-to-date.

The S&P 500? Down 6.4%.

That’s a nearly 8% spread since the start of the year.

Concentration in a Down Market

When the market sells off, most investors scramble. They rotate into large caps, buy ETFs, hide in cash.

I did the opposite this week. I added to two existing positions.

I’ve written before about Lee Freeman-Shor’s The Art of Execution and the lessons it holds for managing a concentrated portfolio.

One of the core takeaways is simple: when you have conviction in a business and the price drops, you have to be willing to act.

The investors who underperform aren’t the ones who pick the wrong stocks - they’re the ones who freeze when it matters.

So I didn’t freeze.

I doubled down on two positions that I know well, that I’ve followed closely, and where the thesis remains fully intact. Combined, they now make up roughly 14% of the portfolio.

Letting Positions Earn Their Size

I recently re-read an article by Ian Cassel on MicroCapClub about what high conviction actually means in practice. His framing stuck with me.

Most investors hear “high conviction” and think it means taking a massive initial position.

Cassel argues the opposite: high concentration doesn’t mean sizing big at the start. It means letting winning positions get big over time.

These two positions are earning their size. Both companies have delivered on earnings. Both have management teams I back. And both have seen their share prices fall since I first bought them - which, if the thesis is intact, is an opportunity to add, not a reason to run.

In the past, I’ve made the mistake of going too big too early. I had conviction, but volatility meant I overpaid in hindsight. Large initial weightings left me exposed to drawdowns that were harder to sit through - not because the business was wrong, but because I’d overstepped my conviction relative to where I was in the relationship with the company.

That experience changed how I approach position sizing. I now build into positions gradually, letting my conviction scale with the evidence. It’s me evolving as an investor. I start smaller, add as the business proves itself, and let the weighting grow over time rather than front-loading the bet.

That’s exactly what’s happening here.

A Small Addition

On a separate note, I also added a small lottery-type position this week - an idea I came across via Real Economy Ideas.

It’s sized accordingly. As Cassel points out, high conviction doesn’t look the same in every situation. A story stock or speculative position warrants a much smaller allocation than a proven compounder, because the risk profile is fundamentally different. You can have conviction in an idea while still expressing it through disciplined sizing.

The position is tiny. The asymmetry is what makes it interesting.

The Bigger Picture

The fact that this concentrated micro-cap portfolio is outperforming the wider benchmark this year is encouraging. I think it reflects the asymmetry built into a lot of the current positions - businesses that are misunderstood, undervalued, or simply too small for most institutional investors to care about.

That’s the edge. And markets like this are where it shows up.

I’m not celebrating a quarters performance. But I am paying attention to what it tells me about the portfolio’s construction and where the risk-reward sits today.

So far this year, the process is working.

In the rest of this post, I’ll cover the positions I added to, the new weightings for all positions in the portfolio, and a move I’m planning to make next week.