10 Quality Stocks Down Big This Year

Owning great businesses doesn't protect you from large drawdowns. Ten quality names are down 9-30% this year already.

To read our full disclaimer, click here.

So far this year, I’ve found 10 quality stocks that are down between 9% and 30%.

Not speculative names. Not broken businesses. These are companies that have historically been classed among the best in public markets - proven compounders, dominant platforms, serial acquirers with long track records of value creation.

And they’ve been crushed in the first 39 days of the year.

There’s a common assumption among investors that owning “quality” insulates you from large drawdowns.

It doesn’t.

Quality businesses still get hit - by shifting narratives, by macro headwinds, by disappointing guidance - and when they do, the recovery math is punishing.

Below, I walk through each name, what’s driving the selloff, and the return required just to get back to where it started the year.

PayPal - Down 30.48%.

Needs +43.8% to recover.

PayPal is the worst hit on this list. The company announced a CEO transition and followed it with a 2026 outlook that disappointed: flat to low single-digit profit growth versus the Street’s ~8% expectation. Branded checkout growth decelerated, and investors hit the exits.

This is a business that has been in the penalty box for years now. But it remains one of the largest digital payments platforms in the world with hundreds of millions of active users. The question is whether new leadership can reignite growth - and whether a 44% rally from here is even realistic in the near term.

Lumine Group - Down 25.93%.

Needs +35.0% to recover.

Constellation Software - Down 24.87%.

Needs +33.1% to recover.

Topicus - Down 24.25%.

Needs +32.0% to recover.

These three are all part of the same family. Constellation is the parent - arguably the greatest serial acquirer in public markets. Topicus is its European spinoff. Lumine is the communications vertical spinoff. Together, they’ve compounded capital at extraordinary rates for over two decades through disciplined acquisition of vertical market software businesses.

All three are down 24-26% in 39 days.

The culprit is a sector-wide AI panic that has swept through SaaS and vertical market software. The narrative goes: if AI can automate workflows, the niche software businesses these companies acquire become less defensible. Organic growth concerns and a broader tech rotation have compounded the selling.

These companies own hundreds of mission-critical, deeply embedded applications across industries from funeral homes to public transit. Whether the AI narrative is warranted or overblown will take time to play out. In the meantime, each of these names needs a 32-35% gain just to get back to flat.

Adobe - Down 19.48%.

Needs +24.2% to recover.

Adobe’s story is straightforward: AI disruption.

The concern is that generative AI - from image creation to code generation - could cannibalize Adobe’s core creative and document businesses. The fear is that seat-based software licensing becomes less valuable in a world where AI agents can do creative work autonomously.

Adobe has faced existential narratives before. The company successfully transitioned from perpetual licenses to subscriptions a decade ago, and continues to integrate AI into its own product suite. But the market is pricing in disruption risk. Whether that’s warranted depends entirely on execution over the next 12-24 months.

Lululemon - Down 18.01%.

Needs +22.0% to recover.

Lululemon is dealing with a triple whammy: tariff headwinds, a CEO transition (Calvin McDonald departing at the end of January), and weak U.S. comparable sales - down 5% year-over-year. Gross margins contracted meaningfully on markdowns and tariff-related cost pressure.

This is a brand that redefined premium athleisure and built a fiercely loyal customer base. The tariff issue is macro noise - it hits the whole sector. The CEO departure is more concerning, as McDonald was widely credited with the international expansion.

Auto Trader - Down 15.74%.

Needs +18.7% to recover.

Auto Trader was hit by an analyst downgrade and - more interestingly - an unusual dealer revolt. Roughly 165 dealers have cancelled or given notice on contracts in response to mandatory “Deal Builder” product bundling. For a marketplace business, dealer satisfaction is the lifeblood. This bears watching.

Rightmove - Down 13.16%.

Needs +15.2% to recover.

Rightmove continues to face competitive pressure from CoStar’s push into the UK property market. The stock has drifted lower as the market weighs the durability of its near-monopoly position. Rightmove is still the dominant UK property portal - but dominance alone hasn’t been enough to stop the slide.

Uber - Down 9.76%.

Needs +10.8% to recover.

Uber’s selloff was driven by a softer profit outlook rather than any operational deterioration. Revenue growth remains solid and the platform continues to expand. This is the mildest decline on the list - more of a market mood swing than a fundamental shift.

Novo Nordisk - Down 9.07%.

Needs +10.0% to recover.

Novo Nordisk is down despite being the dominant player in the GLP-1 obesity market. The company pre-released 2026 guidance that shook investors: a 5-13% decline in both sales and operating profit. The driver is pricing pressure in the U.S., where competition from compounding pharmacies and the prospect of Trump’s most-favored-nation pricing policy are squeezing margins on Wegovy.

Conclusion

“Invest in quality” might be the most common advice in investing.

And it’s not wrong.

But somewhere along the way, people started treating “quality” like a shield. As if owning great businesses means you’re immune to drawdowns.

You’re not. Every name on this list has historically been considered a quality company.

Strong moats, proven management, durable competitive advantages - none of that stops the market from repricing you 25% lower in a month when the narrative shifts. The business can be excellent and the drawdown can still be brutal.

Those two things coexist all the time.

So how do you navigate it? For me, it comes down to concentration, conviction, and doing the deep work before the drawdown hits - not after. That’s the difference between panicking at -25% and knowing exactly why you own something.

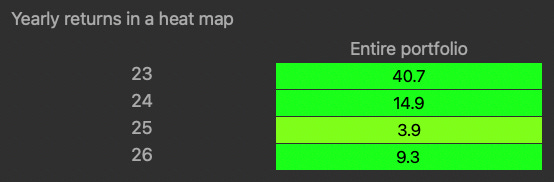

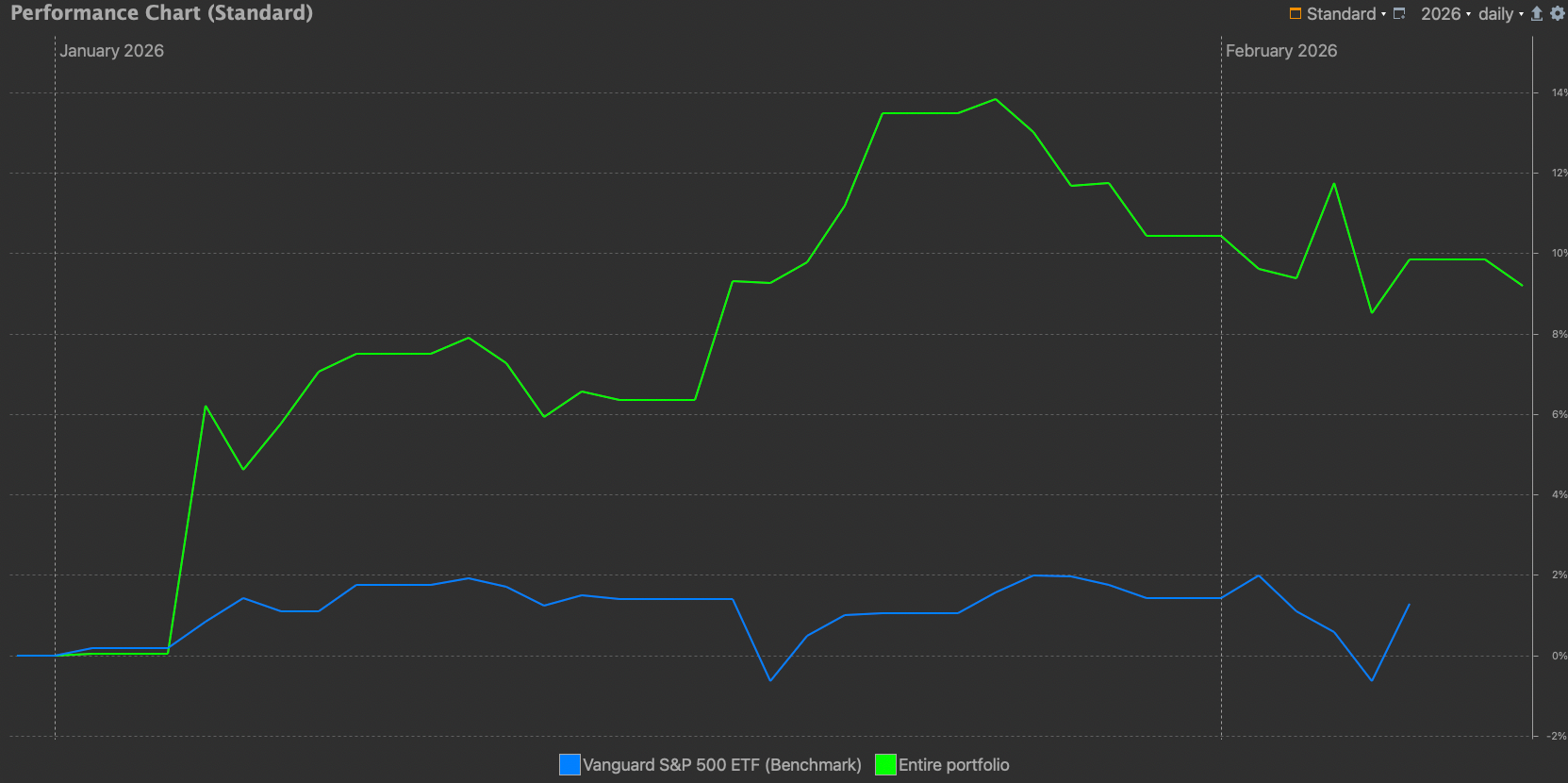

My concentrated portfolio - currently 7 positions, long holding periods, letting winners run - is up 9.3% year-to-date. That’s where I put my own money. That’s where the deep-dive analysis goes.

That’s what paid subscribers get access to.

Thanks for reading,

Dom

Schwar Capital

Disclaimer: The content provided in this newsletter is for informational purposes only and does not constitute financial, investment, or other professional advice. The opinions expressed here are those of the author and do not necessarily reflect the views of Schwar Capital. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. The author may or may not hold positions in the stocks or other financial instruments mentioned. Always do your own research or consult with a qualified financial advisor before making any investment decisions. To read our full disclaimer, click here.

Just short-term noise. We need to take advantage of these types of drawdowns to buy more.